In the 1990s, U.S. companies were among the first to develop and modernize the Central Asian gas and oil industry, remaining today among its largest investors and those most keen to increase their investments. U.S. energy prices were articulated during the campaign as a serious concern to the new administration and are directly linked to Central Asia’s oil market.

Photo: State Department photo by Ron Przysucha

Donald Trump’s new foreign policy agenda, but they won’t be at the bottom either. The first Trump administration was well aware of the region and saw significant promise for U.S. engagement with Kazakhstan, the Kyrgyz Republic, Tajikistan, Turkmenistan, and Uzbekistan. Hosting the presidents of Kazakhstan and Uzbekistan for rare official visits to the White House, the former Trump administration also adopted the 2019-2025 U.S. National Security Strategy for Central Asia – a whole-of-government strategy that has resulted in the region becoming a regular component of U.S. policy, no longer an afterthought. (While a State Department summary is available, the strategy itself remains classified). The Trump-era strategy was adopted unchanged by the Biden administration and remains in effect today and ready to be updated., The Caspian Post reports citing The Diplomat.

Will the approach of the incoming Trump administration toward Central Asia differ much from that of the previous Trump administration? Not likely.

Significant changes have taken place over the last four years in the region since Trump was last in office, but the region’s transformation could work well with Trump’s espoused interests and the likely transactional style of a new Trump foreign policy. Many of the tools and approaches used in the first Trump administration could be reprised to yield significant benefits and a deeper U.S. and Central Asian partnership. The Central Asian states have emerged as a region interested in pursuing efforts to secure their economic sovereignty from neighboring Russia and China. As a result, new opportunities for the United States, particularly in expanding the U.S. business sector in Central Asia, may prove irresistible to the new leadership and its businessman boss.

Understanding the Trump administration’s engagements with Central Asia may be a key to what a new approach might include, particularly as the region has grown increasingly more connected to Europe and less dependent on Russia and China than when Trump was last in office. This new connectivity fits well into the former- and future-president’s actions and efforts in the region, foreshadowing potential early moves with the region once he is re-sworn into office. Energy and strategic minerals are two off-the-shelf standouts for likely attention by Trump’s new Washington team.

A Region of Power

Central Asia’s gas and oil wealth is expected to be a key area of attention for the new Trump administration. A key energy supplier with large reserves, the region is actively working to provide Europe with greater energy independence from Russian supplies. In the 1990s, U.S. companies were among the first to develop and modernize the Central Asian gas and oil industry, remaining today among its largest investors and those most keen to increase their investments. U.S. energy prices were articulated during the campaign as a serious concern to the new administration and are directly linked to Central Asia’s oil market.

The difficult relations between Moscow and Astana and the other Central Asian capitals need to be of interest to the incoming team in Washington. The Central Asian countries feel under pressure from Moscow and are pursuing different courses of action than four years ago. For instance, despite Moscow’s geographic control of most of Central Asia’s energy export infrastructure, Kazakhstan is working to move away from its current pipeline vulnerability. Kazakhstan pumps 80 percent of its oil exports through one Russian terminal. Kazakhstan’s President Kassym-Jomart Tokayev refused in 2022 to support Russia’s war effort in Ukraine, triggering Moscow’s imposition of retaliatory pipeline closures as a direct threat to Astana’s revenue stream. The suspension generated substantial oil price spikes in the tight global oil market and within hours prices at U.S. gasoline pumps rose over a dollar a gallon. Kazakhstan immediately began to pursue alternatives and has not looked back.

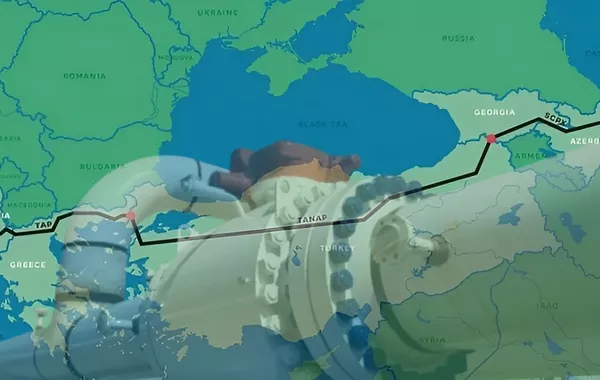

The resulting increased cooperation between Kazakhstan and Azerbaijan to move oil and other goods by sea, along with rumors of their interests in developing a trans-Caspian oil pipeline, are a direct consequence of Russia’s actions. The emergence of the Middle Corridor trade route through the region and across the Caspian Sea is also an outgrowth of increased regional cooperation that seeks alternatives to engagement with Russia.

These developments since the last Trump administration create an opportunity for the incoming administration to help the region secure its economic self-reliance and reduce its dependence on Russia and China by building markets to the West.

A first step for Washington might be to pick up where it left off in 2021, when the Trump administration expressed support for the development of a trans-Caspian gas pipeline connecting Turkmenistan to Azerbaijan, in a strategy that would support both greater energy independence from Russia for Europe as well as greater market resilience and diversity for Central Asia. While this effort was heralded in a 2019 holiday letter to then-Turkmen President Gurbanguly Berdimuhamedov, Ashgabat did not act on the U.S. outreach. Trump reiterated the hope that Turkmen gas could soon be shipped to Europe in a subsequent effort in 2020.

Coming on the heels of the adoption of a long-term, pro-engagement, U.S. National Security Strategy for Central Asia, these pipeline messages suggested Trump’s interest in defining U.S. national interests in the region through a business-oriented approach that would use energy as a major entry point. The opportunity to engage on a trans-Caspian pipeline continues to exist, as gas is regarded as a necessary transition fuel for many European capitals to achieve climate energy objectives. Increased gas sales to Europe would transform Central Asian economies, as happened in the 2000s in the Caucasus when U.S. efforts were instrumental in creating a pipeline for the region’s gas to reach European markets.

To facilitate just this type of major investment lift, the first Trump administration’s Development Finance Corporation (DFC) opened in 2020 and was utilized in Central Asia to leverage U.S. political and financial support for strategic projects. The new administration will likely seek to extend its foreign policy reach by re-energizing DFC’s work as a tool for blending private equity and investment funding to augment U.S. financing of key projects. One immediate step could be through revisiting the DFC Memoranda of Understanding with Kazakhstan and Uzbekistan signed at the end of the Trump administration for $1 billion which were not implemented by the Biden administration.

A trans-border pipeline project would achieve Trump’s long-term objectives of driving down high prices across tight global energy markets, supporting the U.S. gas and oil industry (already operating in the Caspian region), and using U.S. infrastructure investment to deepen cooperation, collaboration, and stability in Central Asia. The five-year DFC agreements were the largest United States government-led initiatives in the region at the time and specifically targeted to support energy connectivity and private-sector development. Welcomed then by the region, the DFC memoranda are still on the table.

Rock Solid Opportunities

Another potential Central Asia policy kickstarter for the new administration is strategic mineral development. The first Trump administration was highly interested in developing and securing stockpiles of strategic and rare earth minerals, declaring the lack of domestic capabilities and reliance on China as a national security threat. To compete with and decouple from China, the administration then even proposed purchasing Greenland as a source of rare elements critically needed for the U.S. economy.

China’s growing monopolization of strategic mineral sources and processing, along with its potential to weaponize its advantage in this field, will undoubtedly be a serious concern for the new administration. Vital to defense and semiconductor industries, as well as the traditional and renewable energy sectors, the abundance of critical minerals in Central Asia remain largely undeveloped. The region’s leaders seek investment and capacity-building to further a more independent course of economic development that is not controlled by Beijing or Moscow. The region contains massive rare earth and other mineral deposits, including 38.6 percent of global manganese ore reserves, 30.07 percent of chromium, 20 percent of lead, 12.6 percent of zinc, 8.7 percent of titanium, and significant reserves of other materials. The United States Geological Survey has been active in the region, documenting significant “occurrences” of these elements in all Central Asian countries.

U.S. businesses are already active in Central Asia’s mining sector, consumers of the region’s critical titanium and uranium deposits, but greater inroads are possible as the U.S. has already initiated a process to develop a partnership in this sector during the Biden administration. The rare earth and strategic mineral sector is critical to U.S. industry and will predictably be a focus of the new administration to rebuild and onshore. As the U.S. looks to nuclear energy under the new administration, Kazakhstan is a global player, producing over 40 percent of the world’s production.

However, though some related mining can be reconstituted within the U.S. and its territories, other scarce materials will require a reliance on partner countries. Priority DFC funding by the new Trump foreign policy team can serve to bolster closer relations with Central Asia as a reliable alternative to their large neighbors, solidify U.S. supply chains of needed and critical commodities, and even deny China access to the region’s vast reserves.

Energy and strategic minerals are a potential cornerstone of reconstituted Trump administration outreach to Central Asia. The explosive growth of the Middle Corridor is a game-changer since Trump was last in office, making transit of goods from this region more reliable, cost-efficient, and accessible to global markets. This transit gateway provides the basis for the region’s long-term economic development and a potential hub for U.S. business investment. The Central Asian countries continue to engage with their neighbors but are more interested in pathways that enable them independent access to global markets. This is a sweet spot for the new administration, particularly as it has a long-term, positive track record of engagement with the region.

Picking up Where He Left Off…

The new Trump administration will have a lot on its plate after taking office. Central Asia will be somewhere on its to-do list, but there are many good reasons for the United States to secure easy wins with the region early on. Energy and strategic minerals will be agenda priorities for a Trump administration, as they were last time. And, just as last time, the region will be anxious to work with the new U.S. team.

In 2018, Trump sent Commerce Secretary Wilbur Ross to Kazakhstan to head a globally rare official trade mission to boost U.S. investment in Kazakhstan and to Uzbekistan to meet with government and business leaders to encourage further trade reforms and World Trade Organization (WTO) accession. His administration focused significant economic development attention on the Central Asian region, including through repeated engagement by the commerce secretary with the region, State Department Secretaries Rex Tillerson and Mike Pompeo’s high-level regional engagements on economic reform, increased funding for the U.S. Agency for International Development’s WTO accession assistance programming and its flagship Central Asia Trade Forum, and increased attention from the U.S. Trade Representative and the United States-Central Asia Trade and Investment Framework Agreement Council. These same tools are still available to Trump and able to take advantage of the region’s increasingly positive trade and development trajectory.

While tied down by other priorities, a new president can achieve much in the foreign policy realm through signaling and empowering U.S. business interests. Continued high-level engagement with the region’s leaders will be important, including early planning for a potential Trump visit to the region that would be a historic opportunity to demonstrate U.S. interest in developing a deeper, sustained relationship. Central Asia is one region that a U.S. president has never visited.

While the expanding connectivity in Central Asia offers many areas for the new Trump administration to work with the region’s countries, working to expand Central Asia’s energy connectivity directly to global markets will both enable these countries to have greater control of their economies, but also help reduce and stabilize global energy pricing – undoubtedly a key concern for the Trump team. Energy and strategic mineral development in Central Asia can be a massive opening for U.S. business to further invest and develop resources that are crucial to the U.S. economy and to developing the region’s economic sovereignty. Engaging the region through Trump’s own DFC initiative can provide significant catalyzing power for U.S. business and industry, working to turn this crossroads region into a dynamic hub.

The Central Asian nations are no strangers to the Trump White House. The new Trump administration will have many opportunities for partnering with this strategic region, which is already reaching across the Caspian in a bid to boost trade and connectivity. Possessing massive traditional and next-generation energy resources and burgeoning economies, Central Asia shares many areas of potential mutual interest with the U.S., which is reason enough for Trump officials to engage with the region sooner rather than later. The key question will be where to start first.